Tencent Holdings (0700.HK): AI Strategy, Value Capture, and the Agent Era

A first-principles analysis of Tencent's AI strategy, exploring how WeChat's distribution, mini-program execution layer, payment infrastructure, and cloud services may convert AI capability into long-term free cash flow.

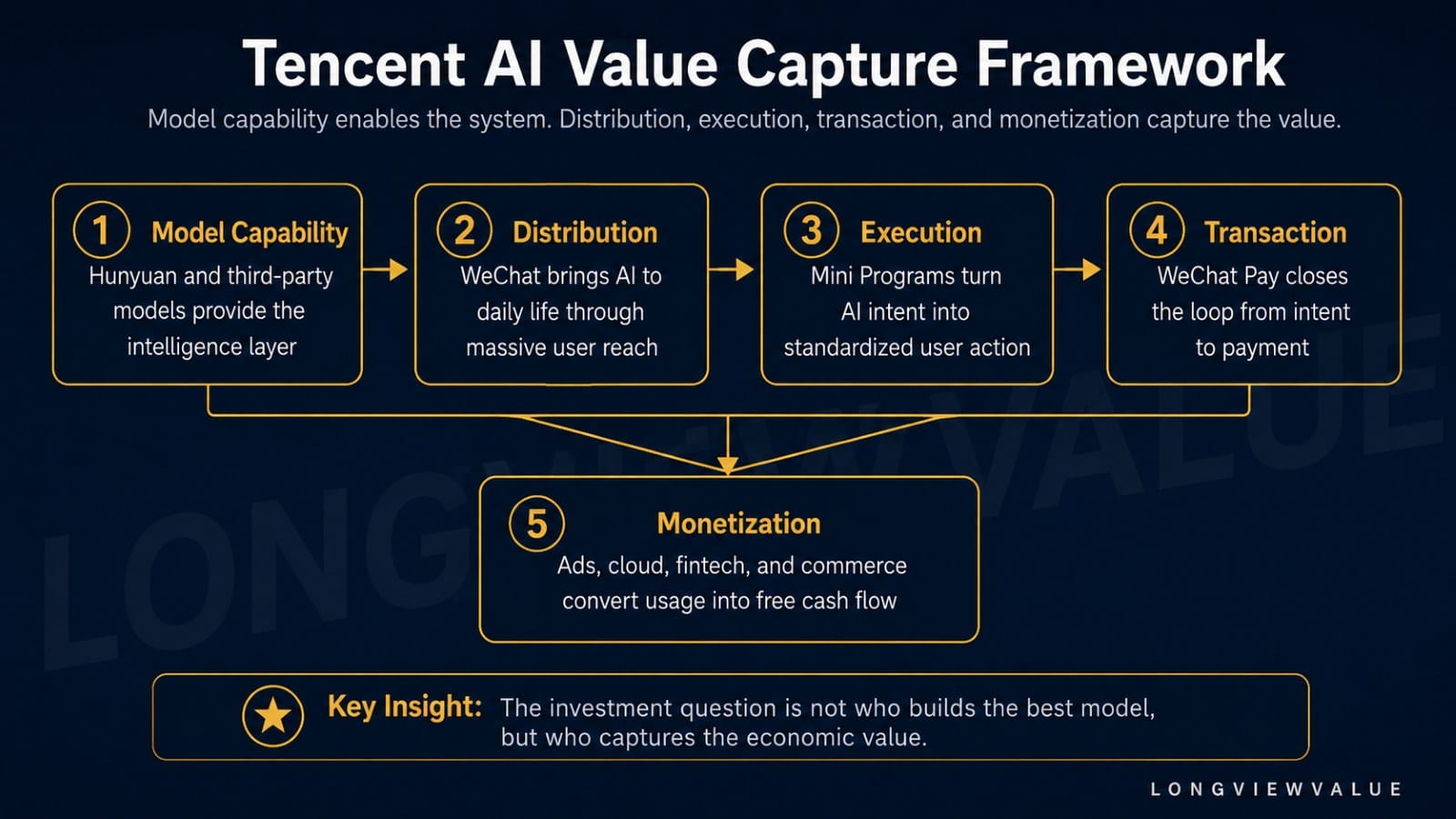

How Tencent's WeChat ecosystem may convert AI capability into distribution, execution, transactions, and long-term free cash flow.

The market counts models.

The rigorous investor counts distribution.

This is Part 3 of the LongViewValue Tencent Research Series, following the Investment Thesis and Economic Moat chapters.

Tencent's Pragmatic AI Approach

There is a particular kind of intellectual discipline required to evaluate a technology company's artificial intelligence strategy without being seduced by the narrative. The AI arms race among Chinese internet giants has generated enormous quantities of commentary — most of it focused on model benchmarks, parameter counts, and the theatrical cadence of product launches. Very little of it asks the more fundamental question that long-term investors should be asking: which company is structurally positioned to convert AI capability into durable, high-margin Free Cash Flow (FCF)?

Tencent's AI strategy, examined through this lens, reveals something that the benchmark-obsessed coverage almost entirely misses. Tencent is not competing to win the large language model race in the way that a pure-play AI lab might. It is competing to win the application layer — the layer where AI transitions from an impressive demonstration into a closed-loop commercial transaction embedded inside the daily lives of 1.4 billion users. That is a fundamentally different game, and it is one that Tencent's existing infrastructure is uniquely equipped to play.

Model capability is not the same thing as economic value capture.

The company's approach is best described as pragmatic sequencing. Management has been explicit: 2025 AI-related investment reached RMB 18 billion, and the company has committed to more than doubling that figure in 2026. Yet this capital deployment is not being directed primarily at frontier model research for its own sake. It is being directed at three interlocking objectives — empowering the advertising stack with AI-driven recommendation efficiency, rebuilding the search and discovery layer inside WeChat, and constructing what management has explicitly called "ecosystem-type Agents" that leverage the mini-program ecosystem, the social graph, and WeChat Pay as an execution layer.

This is a company that has learned, across multiple technology cycles, that the most durable competitive position is rarely held by the first mover. It is held by the platform that waits for the paradigm to clarify, then deploys its existing infrastructure advantages to scale faster than any challenger can replicate. Understanding that pattern — and why it applies with particular force to the Agent era of AI — is the analytical foundation for everything that follows in this chapter.

In This Report

This chapter unfolds through four ideas:

→ Why Tencent is not competing to win the model race

→ Why WeChat may become the operating system of the Agent era

→ Why Alibaba and DeepSeek represent different competitive layers

→ How the bull, base, and bear cases are structured

→ The bull case: three asymmetric monetization catalysts

→ The bear case: CAPEX pressures and user time dilution

→ Why AI may function as a high-margin option rather than a priced-in certainty

The central question is not whether Tencent can build the most powerful model.

It is whether Tencent can convert AI capability into distribution, execution, transactions, and ultimately free cash flow.

The framework below summarizes that value-capture logic.

Cutting Through the Hype: Hunyuan 3.0 and WeChat AI Agents

The Hunyuan 3.0 Milestone in Context

In April 2026, Tencent released the Hunyuan 3 Preview model, built on a fast-slow fusion Mixture-of-Experts (MoE) architecture. The headline metric that captured market attention was its ranking: upon release, Hunyuan 3 Preview achieved the top position in token usage on OpenRouter, the third-party model aggregation platform that serves as a relatively unbiased proxy for real-world developer adoption. This is a meaningful data point, but it requires careful interpretation.

The significance of the OpenRouter ranking is not that Tencent has suddenly surpassed every frontier lab in raw capability. The significance is that Hunyuan 3 has crossed a threshold of practical utility — the point at which developers and enterprises find it cost-effective and capable enough to deploy at scale. For a company whose AI monetization thesis rests on enterprise adoption and ecosystem integration rather than consumer subscriptions, this threshold matters far more than any single benchmark score.

Tencent has also built out a complete multimodal model matrix covering text, image, audio-video, and 3D generation. The WorkBuddy enterprise productivity agent has been cited by management as the most widely used productivity AI Agent service in China as of Q1 2026. These are not vaporware announcements — they represent a coherent product architecture that is already generating measurable commercial traction.

The Mini-Program Ecosystem as an AI Deployment Infrastructure

Here is where the analysis becomes genuinely differentiated from anything the mainstream technology press has written about Chinese AI stocks. The WeChat mini-program ecosystem — comprising over 4 million individual mini-programs built by more than 10 million developers — is not merely a distribution channel. In the context of AI Agents, it is a tool library of extraordinary depth and standardization.

When Tencent's management describes their vision for WeChat AI Agents, they are describing a system in which an Agent can call upon any of those 4 million mini-programs as a standardized tool interface. A user asking an Agent to book a restaurant, file an expense report, or research a product does not require the Agent to navigate to an external website or authenticate with a third-party service. The tools are already inside the ecosystem, already authenticated, already connected to WeChat Pay's 1 billion-user payment infrastructure.

In March 2026, Tencent Cloud confirmed that QClaw had been upgraded to a WeChat mini-program entry point, launching a "Inspiration Plaza" with pre-configured task templates across office productivity, deep research, and entertainment scenarios. Management has indicated that the WeChat AI Agent is expected to reach full deployment in Q3 2026. The architecture being built is not a chatbot bolted onto a messaging app. It is an attempt to make WeChat the operating system of the Agent era — with the social graph providing intent understanding, the mini-program ecosystem providing tool execution, and WeChat Pay providing transactional closure.

This is the structural argument for why Tencent's "late" entry into AI is better understood as deliberate positioning rather than competitive weakness. The private domain ecosystem that WeChat has spent fifteen years constructing is precisely the infrastructure that the Agent paradigm requires.

Chatbots compete on eloquence.

Agents compete on execution.

And execution requires exactly what WeChat already has.

Competitive Landscape: Tencent vs. Alibaba and DeepSeek

Why the IaaS Layer Is Not Tencent's Battlefield

A recurring analytical error in coverage of Chinese AI stocks is the conflation of different competitive layers. Alibaba Cloud, with its dominant Infrastructure-as-a-Service (IaaS) position and deep integration with the Alibaba e-commerce data flywheel, is competing on a fundamentally different axis than Tencent. DeepSeek, the Hangzhou-based research lab that captured global attention with its R1 model, is competing on yet another axis — raw model capability and open-source community influence.

Tencent has made a deliberate strategic choice not to compete primarily on the IaaS compute layer. This is not a concession of weakness. It is a rational capital allocation decision rooted in a clear-eyed assessment of where Tencent's structural advantages actually reside.

Consider the economics. IaaS cloud computing is, at its core, a capital-intensive commodity business. Margins are structurally compressed by the need for continuous CAPEX (Capital Expenditures) in server infrastructure, and competitive differentiation is difficult to sustain when the underlying compute is largely fungible. Alibaba Cloud's leadership in this segment reflects years of investment and the natural advantage of serving the Alibaba e-commerce ecosystem's internal demand. For Tencent to attempt to displace Alibaba on this dimension would require enormous capital deployment with uncertain returns — precisely the kind of capital-destructive competition that disciplined long-term investors should be skeptical of.

Tencent Cloud's strategy is instead oriented toward the application and intelligence layer — AI-powered services, Model-as-a-Service (MaaS) platforms like TokenHub, and vertical solutions for industries like financial services, media, and government. This is where Tencent's unique assets — the WeChat ecosystem, the gaming content library, the advertising data flywheel — create genuine differentiation that cannot be replicated by a pure infrastructure provider.

The 2025 milestone of Tencent Cloud achieving RMB 5 billion in adjusted operating profit is significant precisely because it demonstrates that this application-layer strategy is generating real returns. Tencent Cloud has transitioned from a cost center to a profit center, and it has done so without attempting to win a CAPEX arms race against Alibaba or the state-owned telecom clouds.

The DeepSeek Dimension

DeepSeek's emergence as a globally recognized open-source model provider has complicated the competitive narrative for all Chinese AI players. For Tencent specifically, DeepSeek represents both a competitive reference point and a potential partner. In February 2025, WeChat Search integrated DeepSeek R1 to provide AI-powered search functionality — a pragmatic decision that prioritizes user experience over internal model exclusivity.

This integration reflects a broader principle in Tencent's AI strategy: the company is not ideologically committed to using only its own models. The TokenHub MaaS platform explicitly aggregates both proprietary Hunyuan models and third-party models, offering enterprise customers optionality. This is a platform-layer strategy, not a model-layer strategy. The business model being constructed is one where Tencent captures value from the orchestration of AI capabilities within its ecosystem, regardless of which underlying model provides the inference.

For investors evaluating Chinese AI stocks through a long-term compounding lens, this distinction matters enormously. A company that captures value at the orchestration and application layer — where switching costs are high and ecosystem lock-in is structural — is building a more durable competitive position than one that competes solely on model performance, where the frontier shifts every six months.

Recent comments from Tencent’s senior leadership reinforce this interpretation.

At Tencent’s 2026 annual employee meeting, Pony Ma emphasized that Tencent’s AI strategy would follow the company’s own rhythm: steady, product-oriented, and focused on long-term competitiveness and user experience rather than short-term anxiety. In a later public discussion, Tencent’s Chief AI Scientist Shunyu Yao framed the “second half” of AI not as a race to solve already-defined problems, but as a race to identify the right problems, the right contexts, and the right product environments.

This distinction matters.

If the first phase of AI competition was about building increasingly capable models, the next phase may be about embedding those models into real-world workflows, user scenarios, enterprise systems, and transaction loops. That is where Tencent’s existing ecosystem becomes strategically relevant. WeChat distribution, mini-program execution, payment infrastructure, enterprise tools, advertising systems, and cloud services together create a set of contexts that few competitors in China can replicate at similar scale.

In that sense, Tencent does not need to win the model race in every dimension for its AI strategy to create value. The more important question is whether Tencent can become one of the most effective AI distribution and transaction platforms in China.

Institutional Scenario Modeling

The analytical framework developed in the source research constructs three distinct scenarios for Tencent's value trajectory through 2027. Rather than presenting these as price targets, we present them as structured thought experiments — each with explicit assumptions, internal logic, and observable verification signals. The goal is not to predict an outcome but to map the probability-weighted distribution of outcomes and assess whether the current market price adequately compensates for the risk embedded in that distribution.

The base financial parameters are anchored in reported figures: 2025 Free Cash Flow (FCF) of RMB 182.6 billion, 2025 net profit of RMB 224.8 billion (approximately HKD 248.9 billion), and a current market capitalization of approximately RMB 3.5 trillion. The DCF analysis using a 9% equity discount rate and 3% terminal growth rate — applied only to core business cash flows with AI-related incremental CAPEX stripped out — yields an estimated theoretical value range of approximately HKD 658 per share under baseline FCF multiples, representing roughly 45% upside from the HKD 453 reference price embedded in the source analysis.

Critically, that DCF figure excludes any value attribution to the AI strategy. It is, by construction, a floor — the value of the business if AI investment generates zero incremental return. The scenarios below address what happens when AI investment generates returns ranging from transformative to negligible.

The Bull Case: Asymmetric Monetization Catalysts

The bull case rests on three monetization vectors achieving scale simultaneously, each with distinct timelines drawn directly from the catalyst calendar in the source research.

Vector 1: Video Accounts Load Factor Normalization (2027 H1)

Management's own disclosure provides the most precise quantification of this opportunity: Video Accounts currently carry an ad load of 4.5%, which management has explicitly described as "the lowest in the industry." The industry standard for comparable short-video platforms runs at 20% or above. The arithmetic is straightforward — a normalization of the load factor toward even half the industry standard would represent a multi-fold increase in Video Accounts advertising inventory.

The catalyst calendar identifies the Video Accounts ad load adjustment as a Priority 4 event with four-star impact intensity, with the earliest trigger date in H1 2027. The constraint on faster deployment is not commercial — it is the product philosophy that has always governed WeChat's development. Management is acutely aware that over-commercializing the WeChat experience risks degrading the social utility that makes the platform irreplaceable. This is a genuine tension, but it is also a tension that management has navigated successfully across multiple monetization cycles. Video Accounts advertising revenue was already growing at over 50% year-on-year as of the most recent reporting period, and it contributed approximately 35% of total advertising revenue in 2025 — all while carrying the lowest ad load in the industry.

Vector 2: WeChat AI Agent Beta and Full Deployment (2026 Q3 → 2027 Q1)

The WeChat AI Agent represents what the source analysis correctly identifies as the highest-priority catalyst in the entire framework — a five-star impact event with medium certainty, with the earliest meaningful trigger in early 2027. The logic chain is worth stating precisely.

WeChat AI Agents, once fully deployed, will have access to a tool library of 4 million+ mini-programs, an intent-understanding layer built on the social graph of 1.4 billion users, and a payment execution layer through WeChat Pay's 1 billion-user network. No independent AI application — not Kimi, not Doubao, not any standalone chatbot — can replicate this infrastructure in the near term. The competitive moat is not the model; it is the closed-loop execution capability.

The monetization pathway from Agent deployment is expected to catalyze potential growth in at least three revenue streams: direct Agent subscription or usage fees, incremental mini-program transaction volume (and the associated payment processing revenue), and higher-value advertising inventory generated by Agent-mediated purchase intent signals. The 2027 annual report — expected in March 2027 — will be the first opportunity to assess whether this monetization thesis is converting from concept to cash flow.

Vector 3: Cloud Profitability Scaling (2026-2027)

Tencent Cloud achieved RMB 5 billion in adjusted operating profit in 2025, marking its transition from cost center to profit center. Management has guided for "robust" external cloud services revenue growth in 2026 while "sustaining solid profitability and returns." GPU capacity is on track to step up through 2026 and 2027 as domestic AI chip supply constraints ease.

The bull case scenario in the source model assigns 2027 new business revenue of RMB 800 billion at a 20% net margin, combined with RMB 240 billion from legacy businesses, yielding total attributable net profit of RMB 400 billion. At 20x earnings — a multiple consistent with a platform business demonstrating durable AI-driven growth — this implies a market capitalization of RMB 8 trillion, representing approximately 129% upside from the RMB 3.5 trillion base. The source research assigns this scenario a 15% probability, reflecting the genuine uncertainty around AI monetization timelines.

The probability-weighted expected market capitalization across all three scenarios — bull (15%), base (75%), and bear (10%) — computes to approximately RMB 5.085 trillion, representing roughly 45% upside from current levels. This figure is consistent with the DCF floor analysis, providing a degree of cross-validation that strengthens confidence in the directional conclusion.

The Bear Case: CAPEX Pressures and User Time Dilution

Intellectual honesty requires that the bear case receive equal analytical rigor. The source research assigns it a 10% probability, but the underlying mechanisms deserve careful examination because they represent the primary risks to the long-term compounding thesis.

CAPEX Intensity and Non-IFRS Margin Compression

The most immediate financial risk is straightforward: Tencent has committed to more than doubling AI investment in 2026, following RMB 18 billion deployed in 2025. Management has explicitly guided for a "substantial increase in capex, especially in the second half of 2026." The credit period for server supply payments is approximately six days, meaning CAPEX commitments translate rapidly into cash outflows.

In 2024, total CAPEX grew 221% year-on-year and represented approximately 4% of revenue. If 2026 CAPEX scales proportionally with the AI investment doubling commitment, the pressure on Non-IFRS operating margins in the near term is real and quantifiable. The source research notes that the operating cash flow to net profit ratio of 1.35x in 2025 — while excellent in absolute terms — will face compression if CAPEX intensity continues to rise without a corresponding acceleration in AI-driven revenue.

The critical analytical question is whether this CAPEX should be classified as maintenance or growth investment. If AI infrastructure becomes a necessary competitive baseline — analogous to how cloud computing became table stakes for internet businesses in the 2010s — then a portion of this spending will eventually migrate from "growth CAPEX" to "maintenance CAPEX" in any Owner Earnings calculation. That reclassification would reduce the Owner Earnings figure and, by extension, the intrinsic value estimate derived from it.

User Time Dilution and the ByteDance Competitive Pressure

The bear case's second mechanism is more structural and harder to quantify. ByteDance's Douyin platform has been systematically capturing user time at the expense of WeChat's content consumption functions. While WeChat's social utility — the relationship graph that creates irreversible switching costs — is not threatened by Douyin, the content consumption time that WeChat might otherwise capture through Video Accounts is genuinely contested.

The source research acknowledges this tension directly: even with Video Accounts' structural advantages in social sharing and commerce integration, pure content consumption time may not fully displace Douyin's algorithmic recommendation engine. If Video Accounts' user time growth plateaus before the ad load normalization thesis can be fully executed, the revenue upside from that vector would be materially reduced.

The Scenario Parameters

The bear case in the source model assumes AI investment generates essentially zero commercial return, Video Accounts growth stagnates, and the company reverts to a pure mature-business valuation. Under these assumptions, the valuation anchor shifts from earnings multiples to book value. With net assets projected to reach approximately RMB 1.5 trillion by 2027, a 1.5x price-to-book multiple — consistent with the historical trough during the most severe regulatory period of 2021-2023 — implies a market capitalization of RMB 2.25 trillion, representing approximately 36% downside from current levels.

The asymmetry of this distribution — 45% probability-weighted upside against 36% bear-case downside, with the bear case assigned only 10% probability — presents an asymmetrical risk-reward profile under conservative assumptions. The downside is bounded by the extraordinary quality of the core business: a company generating RMB 182.6 billion in annual FCF, with a ROCE (Return on Capital Employed) of 74.2% in 2025, does not trade to liquidation value absent a catastrophic structural impairment of its core franchises.

Conclusion: AI as a High-Margin Option

The analytical framework developed across this chapter leads to a conclusion that is both precise and appropriately humble about its own limitations.

Tencent's AI strategy is not a moonshot. It is not a bet-the-company pivot into an unfamiliar domain. It is the systematic application of a proven competitive playbook — wait for the paradigm to clarify, then deploy existing infrastructure advantages to scale faster than any challenger can replicate — to the most consequential technology transition of the current decade.

The Hunyuan 3.0 model's OpenRouter ranking, the WorkBuddy enterprise Agent's market position, the WeChat AI Agent's Q3 2026 deployment timeline, and the Video Accounts ad load normalization trajectory are not independent data points. They are sequential steps in a coherent monetization architecture that converts AI capability into recurring, high-margin revenue streams embedded within an ecosystem that 1.4 billion users cannot practically exit.

What makes this particularly interesting from a value investing perspective is the structure of the optionality. The core business — gaming, advertising, fintech — generates sufficient FCF to fund the entire AI investment program without impairing the balance sheet or requiring external capital. The 2025 FCF of RMB 182.6 billion comfortably covers the projected 2026 AI investment of approximately RMB 36 billion (double the 2025 figure). This means that the AI strategy is, in financial terms, a free option — the downside of AI failure is bounded by the core business's standalone value, while the upside of AI success is unbounded in the sense that it would represent a structural re-rating of the entire platform.

The DCF analysis quantifies the floor: even under the assumption that AI generates zero incremental value, the estimated theoretical value range based on baseline FCF multiples suggests approximately HKD 658 per share under the 9% discount rate / 3% terminal growth assumption. The current market price, in this framework, is not paying for the AI option at all. It is pricing the core business at a modest discount to its standalone intrinsic value and assigning zero to the ecosystem-type Agent opportunity, the Video Accounts monetization runway, and the cloud profitability scaling trajectory.

For long-term compounding investors, the relevant question is not whether Tencent will win the AI race in the narrow sense of producing the world's most capable language model. The relevant question is whether the WeChat ecosystem's structural advantages — the relationship graph, the mini-program tool library, the payment execution layer — will prove sufficient to capture a disproportionate share of the economic value created as AI transitions from the chatbot era to the Agent era. The historical evidence from three prior technology transitions suggests that Tencent's "late" entries, when backed by this infrastructure, have consistently resulted in durable market leadership.

Business optionality of this quality — where the option is free, the downside is bounded by a world-class cash-generating business, and the upside is a structural re-rating of one of the world's largest digital ecosystems — is rare. It does not appear frequently in the portfolios of investors who require certainty before committing capital. But for those with the analytical framework to distinguish between uncertainty and risk, and the patience to allow the monetization thesis to develop across the 24-to-36-month catalyst calendar outlined above, the structure of this opportunity warrants serious, rigorous attention.

The AI story at Tencent is not yet written. But the infrastructure on which that story will be told has been under construction for fifteen years. That is the most important fact in this analysis — and it is the one that the benchmark-obsessed coverage of Chinese AI stocks most consistently fails to appreciate.

Final Thought

The AI story at Tencent is not yet written.

But the infrastructure on which that story will be told has been under construction for fifteen years.

Tencent Research Hub

This article is part of the LongViewValue Tencent Research Series.

Published

✓ Tencent AI Strategy (Current Article)

Coming Next

→ Tencent Capital Allocation

→ Tencent Valuation

← Back to Tencent Research Hub

Disclosure & Disclaimer

All financial figures are sourced from publicly available Tencent Holdings (00700.HK) earnings releases, management presentations, and analyst call transcripts.

RMB/HKD conversions use an approximate rate of 0.92 unless otherwise noted.

All scenario analyses and DCF estimates represent the author's independent modeling and are subject to material error.

This report is for educational and informational purposes only and should not be construed as investment advice, investment research, a securities recommendation, or an offer to buy or sell any security.

Investors should conduct their own due diligence and consult qualified professionals before making investment decisions.