Tencent Holdings (0700.HK): The WeChat Moat, Capital Discipline, and the AI Option Nobody Has Fully Priced

A value investing analysis of Tencent Holdings (0700.HK), exploring its WeChat moat, capital allocation discipline, AI optionality, valuation, and long-term intrinsic value.

"The moat is not the product."

"The moat is every relationship inside the product."

Introduction

Tencent is one of the most important businesses in China and, in our view, one of the highest-quality companies in the world.

Yet despite its scale and influence, Tencent is often misunderstood by investors.

Many analyses focus on quarterly earnings, regulatory developments, or short-term market sentiment. While these factors matter, they often obscure the more important question:

What makes Tencent an exceptional business over the long term?

This research series approaches Tencent through the lens of value investing.

Rather than attempting to predict short-term stock movements, we seek to understand the underlying drivers of intrinsic value and long-term shareholder returns.

Our analysis is organized around four core pillars:

- Economic Moat — Why WeChat's relationship network may be one of the strongest competitive advantages in the digital economy.

- AI Strategy — How Tencent's ecosystem could create unique opportunities in the emerging AI era.

- Capital Allocation — Management's record of converting free cash flow into long-term shareholder value.

- Valuation — Estimating intrinsic value through earnings power, free cash flow, and sum-of-the-parts analysis.

Together, these pillars form our investment thesis:

Tencent combines a durable competitive advantage, disciplined capital allocation, and significant optionality from AI, while trading at a valuation that may not fully reflect its long-term earning power.

This article serves as an overview of that thesis.

Each pillar is explored in greater depth in the accompanying research notes.

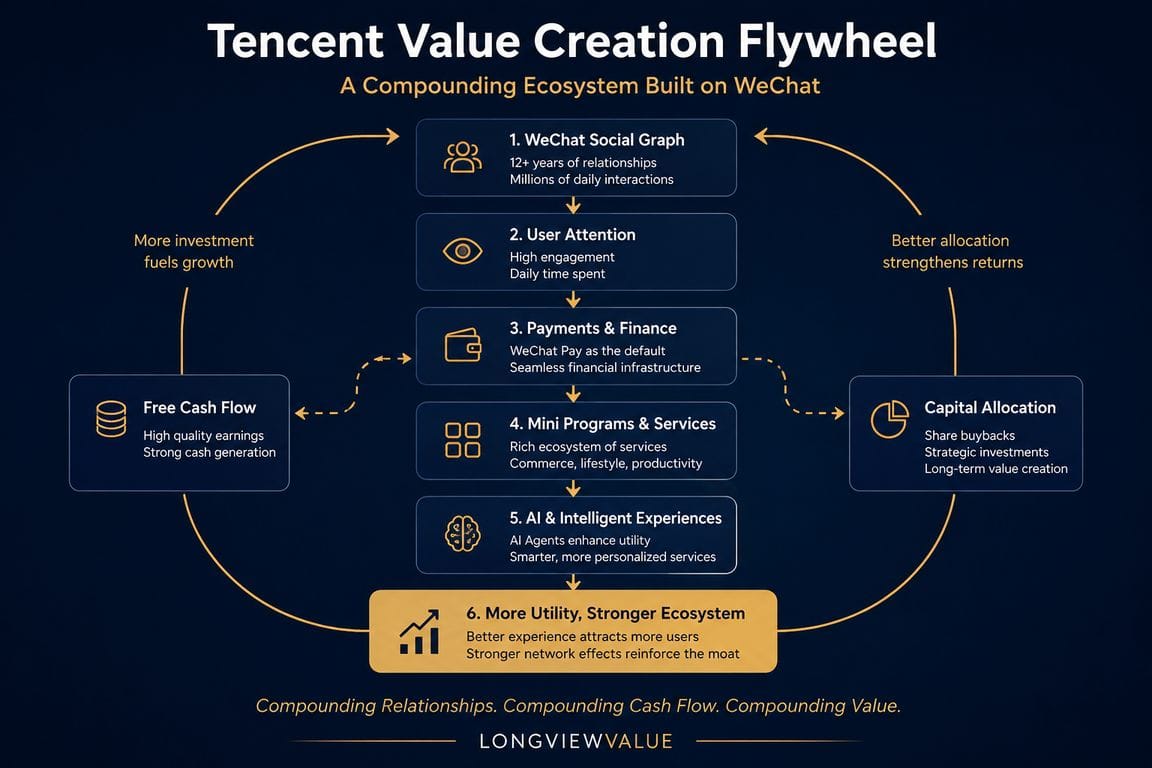

Tencent Value Creation Flywheel

Figure 1. Tencent's value creation flywheel. WeChat's relationship graph strengthens monetization, generates cash flow, funds reinvestment and buybacks, and creates optionality for future AI-driven growth.

Key Takeaways

- WeChat's relationship graph represents a unique and highly durable competitive moat.

- Tencent generated RMB 182.6 billion of Free Cash Flow in FY2025.

- The company continues to demonstrate institutional-grade capital allocation discipline.

- Current valuation remains near historical trough levels despite improving fundamentals.

- AI optionality provides meaningful upside without being required for the investment thesis to work.

- The combination of quality, valuation, and optionality creates an attractive long-term investment profile.

In This Report

- Executive Summary

- Business Overview

- Core Investment Thesis

- The WeChat Moat

- Institutional-Grade Capital Allocation

- AI and Video Accounts as Asymmetric Options

- Deep Margin of Safety Anchored by PB Multiples

- Conclusion and Outlook

Executive Summary

There is a particular category of business that long-term, first-principles investors find most intellectually compelling:

one where the core economic engine is structurally protected, the financial statements are nearly impossible to manipulate, and the market's current pricing reflects fear rather than fundamentals.

Tencent Holdings, in our analytical framework, presents precisely this configuration.

The Tencent investment thesis rests on a deceptively simple foundation.

At its core sits WeChat — a platform with over 1.4 billion monthly active users (MAU) whose economic moat is not derived from network effects in the abstract, but from something far more durable:

the irreversible accumulation of every user's entire social graph within a single ecosystem.

Family, colleagues, clients, acquaintances from a single conference encounter — all of them exist, and only exist, inside WeChat.

This is not a switching cost.

It is a switching impossibility.

That structural anchor underwrites everything else.

Tencent's traditional businesses — gaming, digital advertising, and FinTech — generated RMB 224.8 billion in attributable net profit in 2025, a figure that represents a 10-year compound annual growth rate of 20.7% and has never once turned negative, even during the most severe regulatory tightening cycle China's internet sector has experienced.

The operating cash flow-to-net profit conversion ratio stood at 1.35x in 2025, confirming that the accounting earnings are not a fiction.

Free Cash Flow (FCF) reached RMB 182.6 billion in the same year.

Key Observation

Tencent is not merely generating accounting profits.

Tencent is converting profits into real cash at scale.

This distinction becomes critically important when assessing long-term intrinsic value.

Against this backdrop of structural cash generation, the market is currently pricing Tencent at approximately 3.24x Price-to-Book — a level that sits in the historical 10th to 15th percentile of the past decade.

Our simplified FCFE discounted cash flow model, deliberately constructed to exclude any AI-related upside, produces an implied value per share under the baseline DCF and P/B scenario of approximately HK$658 per share under base-case assumptions (Ke = 9%, g = 3%), representing roughly 45% above the current price of HK$453.

Even under the most conservative parameterization (Ke = 10%, g = 2%), the model yields HK$520 per share — still above current levels, and still without attributing a single dollar of value to the AI strategy.

That AI strategy — encompassing the Hunyuan large language model, Video Accounts monetization, and Tencent Cloud's transition from cost center to profit center — constitutes what we characterize as a set of asymmetric options layered on top of an already-defensible core business.

The estimated theoretical value range based on baseline FCF multiples does not require AI to succeed.

But if it does, the upside scenario in our probability-weighted analysis implies a market capitalization of RMB 8.0 trillion — more than double today's level.

Investment Implication

The investment thesis does not depend on AI success.

The core business alone appears capable of supporting a valuation materially above current market levels.

AI simply adds a layer of asymmetric optionality.

This is the architecture of the Tencent investment thesis:

a quality business generating structural cash yield, trading at a notable margin of safety based on historical valuation percentiles, with three distinct AI-driven growth vectors that the market has not yet fully incorporated into its pricing.

Business Overview

Tencent Holdings Limited (0700.HK) is a China-domiciled investment holding company headquartered at Tencent Binhai Towers, 33 Haitian Second Road, Nanshan District, Shenzhen, Guangdong Province.

The company operates across three primary reporting segments:

- Value-Added Services (VAS)

- Online Advertising

- FinTech & Business Services

Scale and Financial Snapshot (FY2025)

| Metric | Value |

|---|---|

| Total Revenue | RMB 751.8 billion (HKD 832.3 billion) |

| Revenue Growth (YoY) | +13.9% |

| Attributable Net Profit | RMB 224.8 billion (HKD 248.9 billion) |

| Net Profit Growth (YoY) | +15.9% |

| Operating Cash Flow | RMB 303.1 billion |

| Free Cash Flow (FCF) | RMB 182.6 billion |

| Total Assets | RMB 2,039 billion |

| Gross Margin | 56.2% |

| Net Margin | 29.9% |

| ROE (2025) | 21.1% |

| ROCE (2025) | 74.2% |

| PB (Current) | ~3.24x |

| PE (TTM) | ~15.68x |

| EV/EBITDA | 12.6x |

Key Observation

Tencent is not merely a large technology company.

It is a highly profitable, cash-generative ecosystem business operating at enormous scale.

The combination of:

- 21.1% ROE

- 74.2% ROCE

- RMB 182.6 billion FCF

places Tencent among a relatively small group of global businesses capable of compounding capital at high rates over long periods.

Segment Architecture

The VAS segment encompasses both domestic and international gaming (including titles such as Honor of Kings and PUBG Mobile), social platforms (WeChat and QQ), and digital content subscriptions.

The Online Advertising segment is driven by WeChat Moments, Mini Programs, Video Accounts, and the broader social ecosystem.

The FinTech & Business Services segment covers WeChat Pay, wealth management platform LiCaitong, and Tencent Cloud enterprise services.

Q1 2026 Update

Revenue grew 9% year-on-year to approximately RMB 196.5 billion, demonstrating continued momentum into the current fiscal year.

Investment Portfolio

As of December 31, 2025, Tencent's investment portfolio was valued at approximately RMB 913.8 billion.

This represents:

- 44.8% of total assets

- A significant component of intrinsic value

- An asset base often ignored by traditional valuation frameworks

Why This Matters

Many investors evaluate Tencent solely through earnings multiples.

However, Tencent is not merely an operating business.

It is also one of China's largest corporate capital allocators.

Ignoring the investment portfolio risks understating intrinsic value.

Core Investment Thesis

To formally ground this analysis in data-driven terms, our macro framework conceptualizes Tencent's valuation through a unified, three-pillar value creation system:

- The WeChat Infrastructure

- Capital Discipline

- Unpriced AI Optionality

This framework is evaluated through four critical pillars.

Each pillar stands on its own merits.

Combined, they form a compounding system that may create substantial long-term shareholder value.

The WeChat Moat

The moat is not the product.

The moat is every relationship inside the product.

The concept of an economic moat, as articulated by Warren Buffett, refers to a durable structural advantage that protects a business from competitive erosion.

Most moats are quantifiable:

- Cost advantages

- Scale efficiencies

- Proprietary technology

WeChat's moat is something rarer and more profound.

It is sociological.

Relationship Graph Deposits

Consider the mechanics.

A user who has spent five years on WeChat has not merely accumulated a contact list.

They have embedded their entire social existence into a single platform:

- Family group chats

- Professional relationships

- Payment habits

- Service subscriptions

- Work collaboration threads

The chat history with a business partner.

The shared album with a spouse.

The neighborhood committee group.

The client met once at a conference whose WeChat ID remains the only point of contact.

All of these constitute what we term a:

Relationship Graph Deposit.

Every passing month deepens that deposit.

For all practical purposes, it is non-transferable.

The Hidden Moat Behind 1.4 Billion MAU

This is the micro-level reality that aggregate MAU statistics fail to capture.

WeChat's 1.4 billion MAU figure is impressive.

But the true competitive barrier is not the number itself.

The true barrier is that each of those 1.4 billion users has constructed an irreplaceable personal social infrastructure on the platform.

Historical challengers — Alibaba's Laiwang, ByteDance's Duoshan, and others — have all failed to dislodge WeChat.

Not because they lacked features.

But because they could not offer users a mechanism to migrate their relationship graphs.

The moat is not the application.

The moat is every relationship inside the application.

The Strategic Advantage of the Second Mover

This structural reality confers upon Tencent a strategic luxury that few technology companies possess:

the freedom to be a deliberate second mover.

Because WeChat's user base cannot be meaningfully eroded by competitors, Tencent does not need to be first in every technology cycle.

It can observe.

It can wait.

It can allow the market to validate a technology paradigm.

And then it can deploy its distribution infrastructure at scale.

The historical record is unambiguous.

PC to Mobile

WeChat launched in 2011, after competitors like Xiaomi's MiChat.

By leveraging QQ's existing relationship graph, it achieved 100 million users within a year and became the defining platform of China's mobile internet era.

Short-Form Video

Video Accounts launched in 2020, four years after Douyin and nine years after Kuaishou.

Yet by 2025, Video Accounts had become China's second-largest short-video platform by time spent, with usage time growing more than 20% year-on-year.

Artificial Intelligence

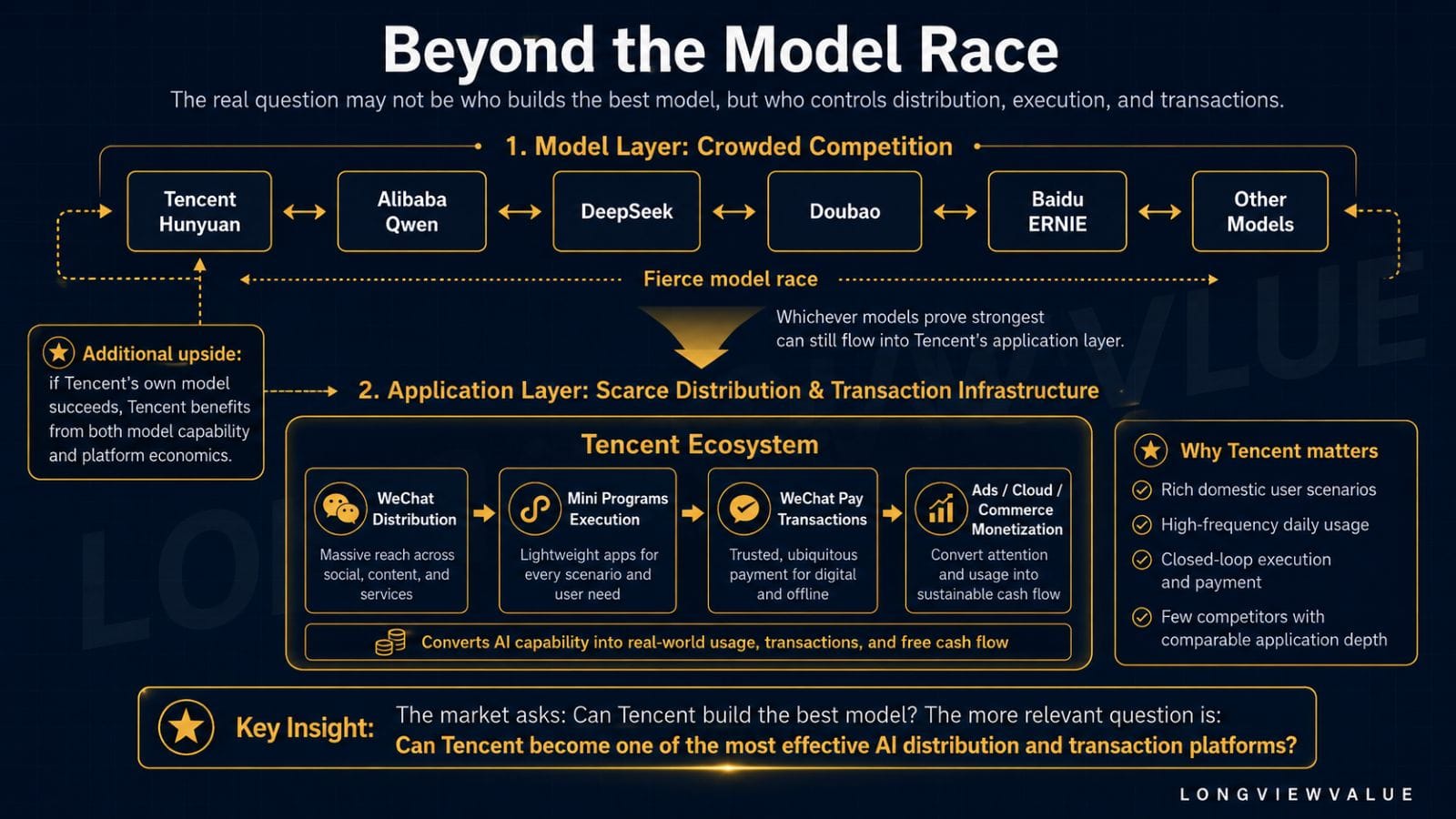

The current market narrative that "Tencent is moving slowly on AI" is, in our analytical view, a misreading of a deliberate strategic posture — one that has been validated twice before in living memory.

Investment Implication

When evaluating Tencent's AI competitive position, the relevant question is not whether Hunyuan was the first large language model released in China.

The relevant question is:

Can Tencent embed AI capabilities into the WeChat ecosystem at sufficient depth and speed to convert 1.4 billion social relationships into AI-mediated commercial transactions?

That is a fundamentally different question.

And in our view, it has a fundamentally different answer than the one currently implied by market sentiment.

Institutional-Grade Capital Allocation

The quality of a business is revealed by how it allocates capital.

The quality of management is revealed by what it does with free cash flow.

Charlie Munger observed that the single most important variable in long-term investment outcomes is the quality of capital allocation by management.

A business that generates substantial cash but deploys it poorly destroys value.

A business that generates substantial cash and deploys it with discipline compounds it.

Tencent's capital allocation record warrants careful examination on both dimensions.

The Cash Generation Machine

Tencent's Owner Earnings — the metric Warren Buffett introduced in his 1986 Berkshire Hathaway shareholder letter, defined as net profit plus depreciation and amortization minus maintenance CAPEX minus incremental working capital requirements — have been consistently extraordinary.

Over the three years from 2023 to 2025, the Owner Earnings-to-net-profit ratio ranged from 86.8% to 95.2%.

In 2025:

| Metric | Value |

|---|---|

| Net Profit | RMB 224.8 billion |

| Owner Earnings | RMB 214 billion |

| Conversion Ratio | 95.2% |

Key Observation

Tencent converts accounting earnings into economic earnings at an unusually high rate.

This ratio is a direct measure of business model quality.

A manufacturing company with heavy asset replacement requirements might convert only 30–50% of reported profits into Owner Earnings.

Tencent's 95% conversion reflects the fundamental economics of a platform business.

Once the software infrastructure is built, each incremental unit of revenue — a game purchase, an advertisement impression, or a payment transaction — requires virtually no additional capital investment to service.

The business is, in Buffett's terminology, a "toll bridge" rather than a capital-intensive railroad.

Balance Sheet Strength

The balance sheet reinforces this picture.

Total assets of RMB 2,039 billion are financed with an interest-bearing debt ratio of only 19.9%.

The effective borrowing rate, derived by dividing 2025 financing costs of RMB 15.1 billion by average interest-bearing debt of approximately RMB 381.8 billion, computes to 3.95%.

Meanwhile, the company's cash and cash equivalents and liquid financial assets generate an implied yield of approximately 4.1%.

Why This Matters

Tencent earns more on its cash than it pays on its debt.

That is a rare position for a company of this scale.

It provides management with unusual financial flexibility during periods of uncertainty.

Shareholder Return Discipline

In 2025, Tencent returned approximately RMB 73.4 billion to shareholders through share repurchases — nearly double the RMB 37.6 billion distributed as dividends.

This ratio is not accidental.

At a current PB of 3.24x against a 10-year median of approximately 6.5x, repurchasing shares is mathematically equivalent to acquiring the company's own assets at a substantial discount to historical valuation levels.

Each share retired increases the per-share intrinsic value of the remaining shares.

This is precisely the capital allocation logic Buffett has articulated repeatedly:

When a business trades below intrinsic value, repurchases become one of the highest-return uses of capital available.

The 2024–2025 cumulative repurchase program exceeded RMB 190 billion.

Management has simultaneously committed to more than doubling AI investment in 2026 from a 2025 base of RMB 18 billion.

The ability to execute both simultaneously — aggressive reinvestment and aggressive shareholder returns — is the hallmark of a business with genuine financial strength.

ROCE of 74.2% in 2025 confirms that the capital already deployed continues to generate exceptional returns.

Investment Implication

Tencent's capital allocation framework is not dependent on a single growth initiative.

The company can:

- Return capital

- Invest in AI

- Strengthen the balance sheet

- Continue strategic investment activity

all at the same time.

Few businesses possess that degree of flexibility.

AI and Video Accounts as Asymmetric Options

The investment case does not require AI to succeed.

But if AI succeeds, the upside could be substantial.

The analytical framework we apply to Tencent's new business initiatives treats them as options, not certainties.

An option has a defined cost and an asymmetric payoff profile.

The downside is bounded.

The upside is open-ended.

The relevant question for long-term investors is whether the option premium is reasonable relative to the potential payoff.

Video Accounts: The Undermonetized Asset

The most immediately quantifiable opportunity within Tencent's ecosystem is Video Accounts.

Management disclosed in the Q1 2026 earnings call that Video Accounts' advertising load rate stands at 4.5%, explicitly described as "the lowest in the industry."

Industry peers operate at 20% or higher.

This is not a strategic choice to preserve user experience indefinitely.

It is a sequencing decision.

Tencent has prioritized audience depth before monetization intensity.

The Arithmetic

Video Accounts advertising revenue was growing at more than 50% year-on-year as of 2025.

If the ad load rate were to normalize toward even half the industry standard — 10% rather than 20% — the revenue uplift would be substantial.

Our scenario analysis assumes Video Accounts advertising revenue reaches RMB 200 billion by 2027, up from an estimated RMB 60–70 billion currently.

At a 15% net margin, this single business line would contribute approximately RMB 30 billion in incremental net profit.

At 20x earnings, that would represent approximately RMB 600 billion of incremental equity value.

AI: The Structural Advantage of the Late Mover

The Hunyuan large language model has iterated to version 3.0, employing a Mixture-of-Experts (MoE) architecture.

The Hunyuan 3 Preview model, released in April 2026, ranked first in token usage on OpenRouter since launch.

Yuanbao has achieved the third-highest DAU among AI-native applications in China.

WorkBuddy has become the most widely used enterprise productivity AI agent service in the country.

These developments matter.

But they are not the most important part of the AI thesis.

The Agent Paradigm

In the Chatbot era, competition was defined by model benchmark scores.

In the Agent era, competition is defined by the ability to complete tasks.

An Agent requires:

- A tool library

- User intent context

- Transaction completion capability

WeChat's ecosystem already possesses all three.

- Mini Programs provide the tool layer.

- Social graphs provide intent context.

- WeChat Pay provides transaction execution.

No independent AI application can easily replicate this infrastructure.

Why This Matters

The market often asks:

"Can Tencent build the best model?"

We believe the more relevant question is:

"Can Tencent become one of the most effective AI distribution and transaction platforms?"

Those are fundamentally different questions.

Investment Implication

Management has committed to more than doubling AI investment in 2026.

With RMB 182.6 billion of FCF generated in 2025, Tencent can comfortably absorb this investment.

The risk-reward profile remains asymmetric.

If AI initiatives fail entirely, the core business remains intact.

If they succeed, the upside scenario in our probability-weighted framework implies a market capitalization of RMB 8.0 trillion.

Deep Margin of Safety Anchored by PB Multiples

Price is what you pay.

Value is what you get.

The concept of margin of safety — Benjamin Graham's foundational contribution to investment analysis — requires that investors pay a price sufficiently below intrinsic value to protect against uncertainty and analytical error.

We assess Tencent's valuation through four independent lenses.

Each arrives at a similar directional conclusion.

PB Band Analysis

Tencent's current PB of approximately 3.24x sits in the historical 10th to 15th percentile of the past decade.

Historical context:

| Metric | Value |

|---|---|

| Current PB | ~3.24x |

| Historical Median PB | ~6.5x |

| Historical Floor | ~2.4x |

The current level remains closer to the regulatory-cycle trough than to historical normality.

This is notable because:

- ROE has recovered to 21.1%

- Regulatory pressure has eased

- Cash generation remains robust

Investment Implication

The business appears stronger than the valuation implies.

A recovery to:

- 4x PB implies ~HK$560/share

- 5x PB implies ~HK$700/share

- 6.5x PB implies ~HK$910/share

All remain within historically observed valuation ranges.

DCF Valuation — Core Business Only

Our simplified FCFE model deliberately excludes all AI-related investment and associated future returns.

The base-case adjusted core business FCFE of approximately RMB 226 billion is grown at 10% for three years, then 7% for two years, before applying a 3% terminal growth rate.

Using a 9% equity discount rate produces the following result:

| Component | Value (RMB Billion) |

|---|---|

| Present Value of Explicit Period FCF | 1,142 |

| Present Value of Terminal Value | 3,842 |

| Core Business DCF Value | 4,984 |

| Net Cash | 27.4 |

| Investment Portfolio (50% Discount) | 456.9 |

| Total Equity Value | 5,468.2 |

| Per Share Value | ~HK$658 |

Key Observation

The DCF valuation does not require AI success.

The model assigns no value to future AI monetization.

Yet the implied intrinsic value remains materially above the current share price.

Probability-Weighted Scenario Analysis

| Scenario | Implied Market Cap | Probability |

|---|---|---|

| Optimistic | RMB 8.0T | 15% |

| Base Case | RMB 4.88T | 75% |

| Pessimistic | RMB 2.25T | 10% |

Probability-weighted expected market capitalization: RMB 5.085 trillion.

This represents approximately 45% above current levels.

Owner Earnings Quality

The 95.2% Owner Earnings-to-net-profit ratio in 2025, combined with a 1.35x operating cash flow-to-net profit conversion ratio, confirms that reported earnings are not merely accounting constructs.

The business generates real cash.

And it generates it consistently.

Conclusion and Outlook

The analytical exercise of studying Tencent is, at its deepest level, an exercise in understanding what makes a business genuinely excellent — and what it means to acquire a share of that excellence at a price that does not fully reflect its quality.

The WeChat moat is, in our assessment, the most structurally durable competitive asset in China's internet economy.

It is not a product feature.

It is a sociological phenomenon.

One that has been accumulating for fifteen years and deepens with every passing day.

Final Assessment

Tencent combines:

- A durable economic moat

- Exceptional cash generation

- Disciplined capital allocation

- Significant AI optionality

- A meaningful margin of safety

Few businesses globally possess all five characteristics simultaneously.

Whether the market recognizes that value next quarter or three years from now is unknowable.

What is knowable is the underlying quality of the business itself.

And that quality remains exceptionally high.

Tencent Research Hub

This article is Part 1 of the LongViewValue Tencent Research Series.

Published

✓ Part 1: Investment Thesis — Current article

→ Part 3: AI Strategy, Value Capture, and the Agent Era

→ Part 4: Capital Allocation and Owner Earnings

Coming Next

→ Part 5: Valuation and Margin of Safety

← Back to Tencent Research Hub

Disclosure & Disclaimer

All financial data is sourced from Tencent Holdings public filings, earnings call transcripts, and management presentations.

All valuations represent the author's independent analytical work.

Nothing in this report should be construed as investment advice, investment research, securities recommendation, or an offer to buy or sell any security.

Investors should conduct their own independent research and consult qualified professionals before making investment decisions.