Tencent Holdings (0700.HK): The WeChat Moat

How relationships become infrastructure — and why Tencent's social graph creates switching costs that competitors cannot replicate.

This chapter examines the first-principles architecture of Tencent's economic moat — why it exists, why it compounds, and why it has proven structurally immune to every competitive assault launched against it over two decades.

"WeChat has not merely accumulated users.

It has accumulated relationships — and relationships cannot be migrated."

This is Part 2 of the LongViewValue Tencent Research Series, following the Investment Thesis chapter.

Redefining the Internet Moat

There is a category error that pervades most institutional analysis of Tencent Holdings. Analysts, conditioned by the metrics of Western platform businesses, instinctively reach for monthly active user counts, time-spent statistics, and revenue-per-user ratios when attempting to quantify competitive advantage. These are useful numbers. They are not, however, the right numbers for understanding what makes Tencent's economic moat genuinely extraordinary.

The conventional framework for evaluating wide moat companies in the technology sector tends to focus on one of two structural advantages: either the raw scale of a platform network effect — the idea that a service becomes more valuable as more people use it — or the depth of switching costs that make migration to a competitor economically painful. Most platforms exhibit one of these properties in meaningful degree. The rarest businesses exhibit both simultaneously, in a configuration that causes each to reinforce the other in a self-compounding loop.

WeChat is one of those businesses. But even that framing understates the case.

What the source data from Tencent's own management communications and financial disclosures reveals, when examined through a rigorous value investing lens, is something more structurally profound: WeChat has not merely accumulated users. It has accumulated relationships. And relationships, unlike users, cannot be migrated, replicated, or competed away.

This distinction is not semantic.

It is the entire thesis.

More precisely, WeChat has not accumulated a collection of isolated relationships.

It has accumulated a decentralized relationship network in which each additional connection increases not only the size of the graph, but also the value embedded within it.

This distinction matters because the migration cost arises not from individual contacts alone, but from the interdependence of the network itself.

Understanding how network effects create moats at the level WeChat has achieved requires moving beyond the standard textbook definition. Social network effects, in their most powerful form, do not simply make a platform more useful as it grows. They make the cost of leaving approach infinity for any individual user, regardless of how superior a competing product might be on any objective feature dimension. This is the mechanism that transforms a large platform into a permanent one — and it is the mechanism that has made WeChat the single most durable competitive asset in Chinese internet history.

This chapter is an attempt to explain that mechanism with the precision it deserves.

In This Report

This chapter unfolds through four ideas:

→ Social Graph Encapsulation

→ The Luxury of Late-Mover Advantage

→ WeChat vs. Meta Structural Comparison

→ Relationships Over Users

Social Graph Encapsulation

The headline statistic is well known: WeChat operates with over 1.4 billion monthly active users (MAU), a figure that places it among the largest communication platforms ever constructed. But the MAU figure, taken in isolation, is almost misleading in its simplicity. It describes the size of the network without capturing the depth of the encapsulation that makes that network irreplaceable.

The Sole-Channel Relationship

To understand what genuine social graph encapsulation means in practice, consider the following scenario drawn directly from the source research. The author of the underlying analysis attended a significant industry conference and, in a corridor conversation, exchanged WeChat contact details with a senior figure in their field. No phone number was exchanged. No email address. No LinkedIn connection. The WeChat contact was the sole point of connection between two professionals whose relationship carried meaningful potential value.

This is not an unusual situation in China. It is the universal situation. And it illustrates, with more precision than any aggregate statistic, the nature of the switching cost that WeChat has constructed.

The individual in that scenario cannot migrate to a competing social platform — not because WeChat is technically superior, not because the switching process is administratively burdensome, but because the relationship itself is encoded in WeChat's infrastructure. The contact exists in WeChat's social graph. The conversation history lives in WeChat's servers. The implicit social contract of that professional connection was formed within WeChat's ecosystem. A competing application, however elegantly designed, cannot offer what WeChat offers: the relationship as it already exists.

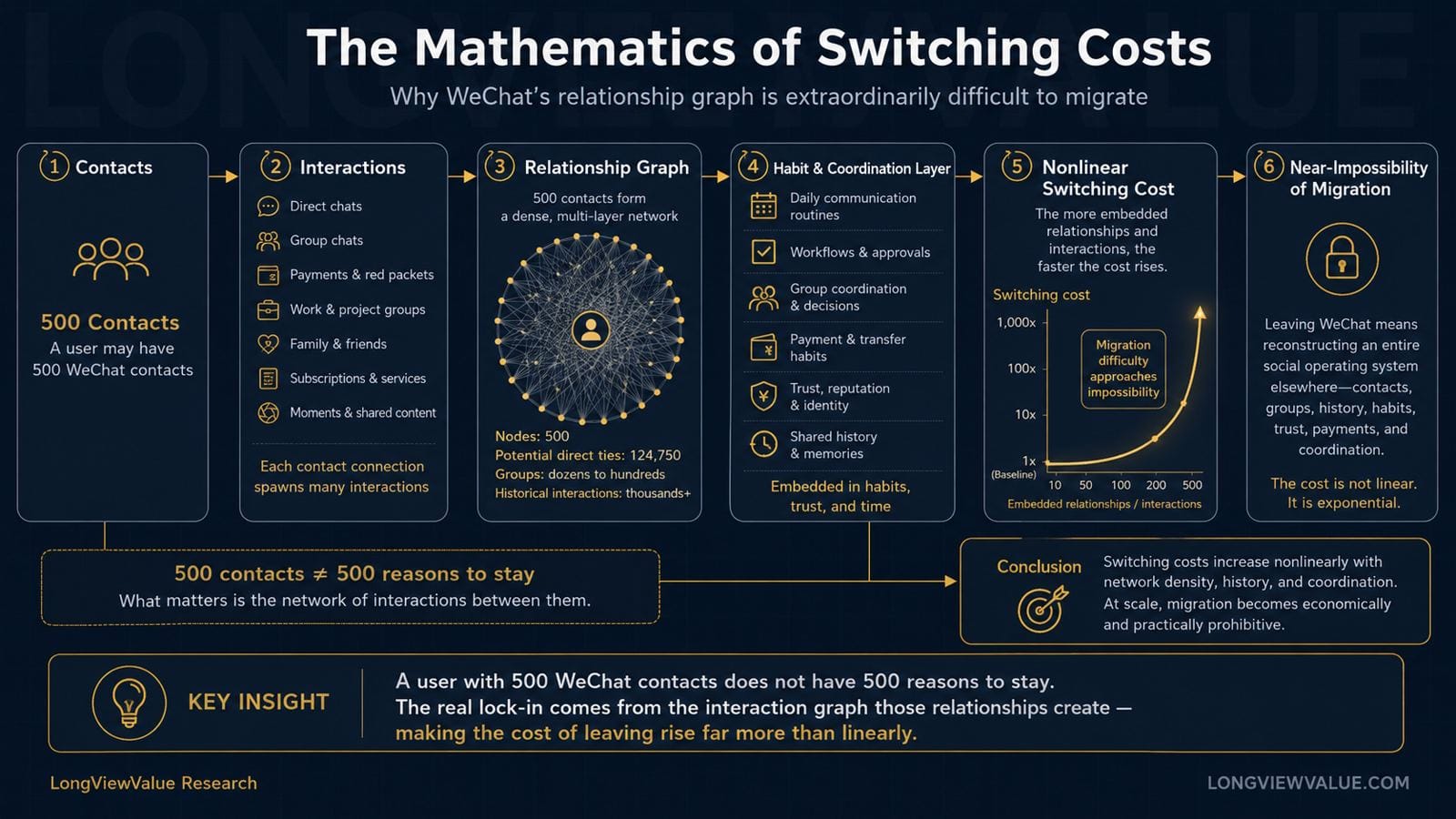

Now multiply that single relationship by the thousands of connections that accumulate in a typical professional's WeChat contact list over a decade of use. Family members. Childhood friends. University classmates. Former colleagues. Current clients. Occasional acquaintances from conferences, dinners, and chance encounters — each one a "sole-channel contact" whose relationship with the user is mediated exclusively through WeChat. The aggregate of these connections constitutes what the source analysis calls a "digital social relationship graph" — a deeply personal, irreplaceable map of an individual's entire social and professional world.

The Mathematics of Switching Costs

This is the architecture of platform network effects at their most powerful. Each new relationship added to a user's WeChat graph increases the cost of leaving not linearly but exponentially, because the value of a social network is not the sum of its individual connections but the product of the interactions between them. A user who has 500 WeChat contacts does not have 500 reasons to stay.

They have something closer to:

500 × 499 / 2 = 124,750 reasons

— one for every potential interaction that would be severed by migration.

Competitive Reality

The historical record validates this analysis with unusual clarity. Over the past decade, a succession of well-funded, technically competent challengers have attempted to displace WeChat as China's primary social communication platform. Alibaba's Laiwang. ByteDance's Duoshan. Luo Yonghao's Chatbao. Each launched with significant capital, credible product teams, and genuine feature differentiation. Each failed to achieve meaningful displacement. The reason was not that WeChat outcompeted them on product quality in every dimension. The reason was that no competing product could offer users their existing relationships. The social graph was already encapsulated. The switching costs were, for all practical purposes, infinite.

This is the Tencent economic moat at its most fundamental level:

Not a product advantage.

Not a technology advantage.

A relationship advantage that has been accumulating, compounding, and deepening for over fifteen years.

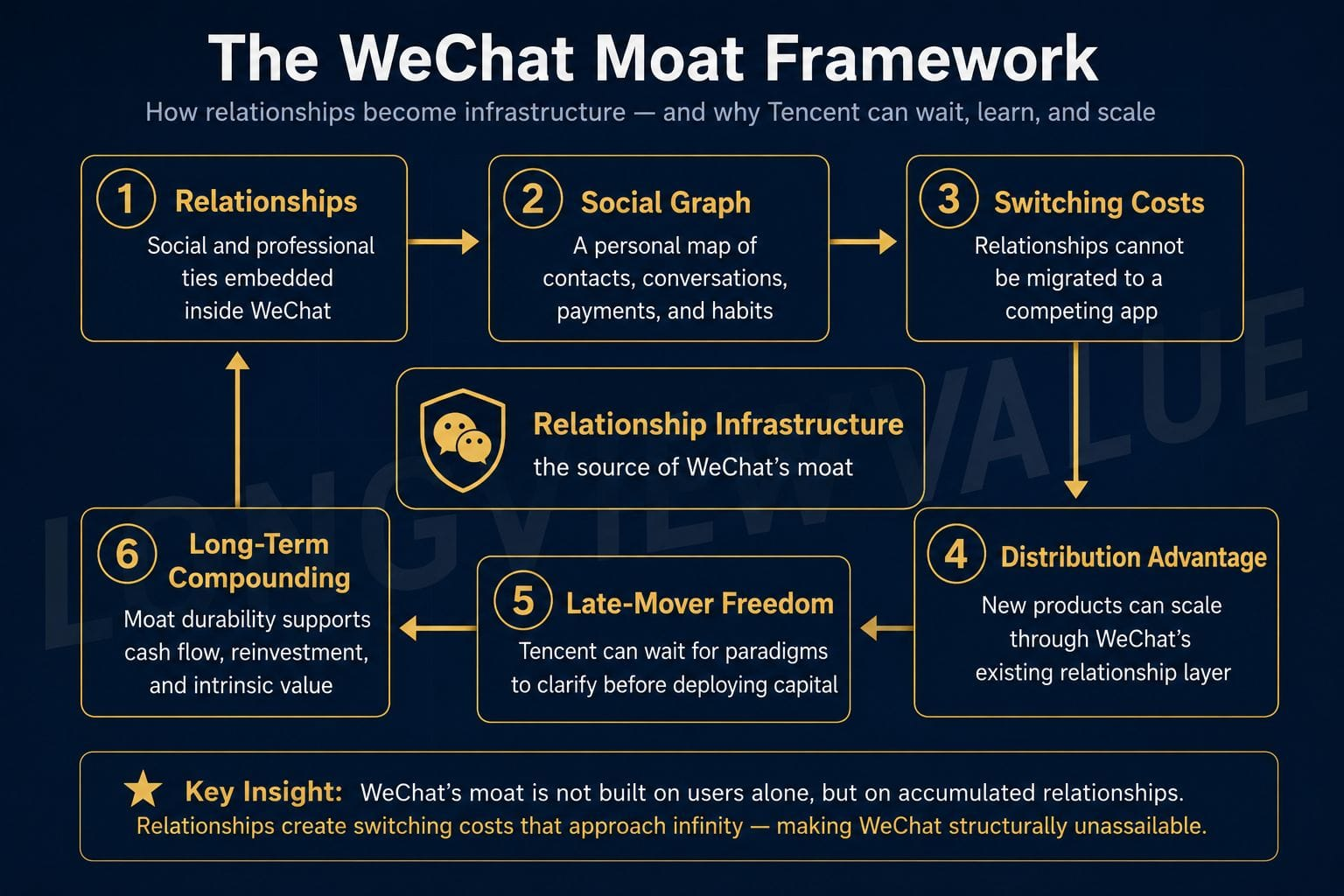

The Luxury of Late-Mover Advantage

One of the most persistent misreadings of Tencent's competitive strategy is the assumption that the company's occasional tardiness in entering new technology categories represents a strategic weakness. The concern surfaces regularly in sell-side commentary: Tencent was late to short video. Tencent appears slow in the AI race. Tencent lacks the first-mover aggression of ByteDance or the research velocity of OpenAI.

This analysis fundamentally misunderstands the strategic logic that WeChat's moat enables. The source material describes this logic with a Chinese phrase — 后发制人 — which translates approximately as "subduing the opponent by striking second." It is not a description of passivity. It is a description of a specific and highly rational competitive strategy available only to businesses that possess an unassailable distribution asset.

Tencent does not have to be first.

It only has to be right.

Why Tencent Can Afford to Wait

The logic works as follows. In any new technology category, the early phase is characterized by high uncertainty about which technical approach will prove durable, which product paradigm will achieve user adoption, and which business model will generate sustainable economics. First movers bear the full cost of this uncertainty: they invest heavily in approaches that may prove to be dead ends, they educate markets that may not yet be ready, and they absorb the reputational and financial costs of public failures. The expected value of first-mover advantage is frequently negative when these costs are properly accounted for.

A company that possesses a distribution asset as powerful as WeChat — 1.4 billion MAU with deeply encapsulated social graphs, a private domain ecosystem of 4 million+ mini-programs, and a payments infrastructure reaching 1 billion users — can afford to wait. It can observe the technology landscape as it clarifies, identify the approaches that are gaining genuine traction, and then deploy its distribution advantage to achieve rapid scale in the validated paradigm. The switching costs that protect WeChat from competitive displacement also provide the runway for this patient, evidence-based approach to new category entry.

The historical evidence for this pattern is compelling across three distinct technology transitions.

Case Study 1 — The PC-to-Mobile Transition

What Happened

WeChat launched in January 2011, meaningfully later than Xiaomi's Miliao and several other mobile messaging competitors. At the time of launch, Tencent's QQ platform had accumulated over 100 million simultaneous peak users on PC — a social graph of extraordinary depth and breadth. WeChat did not attempt to compete with early mobile messaging apps on their own terms. Instead, it leveraged QQ's existing relationship network to achieve cold-start distribution that no competitor could replicate.

Why Tencent Won

Users did not to rebuild their social graphs from scratch; they could import them. By 2012, WeChat had surpassed 100 million users. By 2018, monthly active users exceeded 1 billion. The late entrant became the definitive platform of the mobile internet era.

The first mover educated the market. Tencent inherited the economics.

Case Study 2 — The Short Video Wave

What Happened

Video Accounts launched in January 2020 — approximately four years after ByteDance's Douyin (TikTok's Chinese counterpart) and nearly a decade after Kuaishou. By any conventional measure of first-mover advantage, Tencent had ceded the short video category entirely.

Why Tencent Won

Yet by 2025, Video Accounts had become China's second-largest short video platform by usage time, with year-over-year time-spent growth exceeding 20% and advertising revenue growing at rates consistently above 50% annually. The platform's ad load, at just 4.5% — the lowest in the industry against a sector average above 20% — suggests that the monetization trajectory has barely begun. The late entrant, again, is structurally positioned to mitigate downside risks while retaining enormous upside optionality.

WeChat's moat bought Tencent patience. Patience improved capital allocation.

Case Study 3 — The AI Wave

What Happened

The current market narrative holds that Tencent is "moving slowly" in the AI race, a characterization that management has neither disputed nor been particularly troubled by. The Hunyuan large language model was not among the first Chinese foundation models to market.

Why This Matters

The Yuanbao consumer AI application was not the first Chinese AI assistant to achieve significant distribution. But as of April 2026, Hunyuan 3 — built on a fast-slow fusion Mixture-of-Experts architecture — ranked first in token usage on OpenRouter, the third-party model aggregation platform, since its launch. Tencent's WorkBuddy productivity AI agent has become the most widely used enterprise AI agent service in China. And the WeChat AI Agent infrastructure, expected to reach full deployment in Q3 2026, is expected to catalyze potential growth in a category that no independent AI application can credibly contest — because no independent AI application has access to WeChat's social graph, mini-program tool library, or payments infrastructure.

Investment Implication

The pattern across all three transitions is structurally identical. Tencent absorbs the observation cost of early-stage technology uncertainty, waits for the product paradigm to clarify, and then deploys WeChat's distribution advantage to achieve rapid scale in the validated approach. The strategy is not available to companies without a comparable distribution asset. For Tencent, it is the natural expression of the competitive position that WeChat's social graph encapsulation has created.

The WeChat Moat Framework

WeChat vs Meta Structural Comparison

WeChat is not a messaging application that added features.

It is an operating system for daily life that began as a messaging application.

The most instructive way to appreciate WeChat's structural uniqueness is to compare it directly with the closest Western analog: Meta's messaging and social ecosystem, which encompasses WhatsApp, Facebook Messenger, Instagram Direct, and the Facebook social graph itself.

The comparison is illuminating not because the two companies are similar, but because the ways in which they differ reveal precisely what makes WeChat's competitive position so unusual among global platform businesses.

The Scope of the Operating System

WhatsApp, with approximately 2 billion users globally, is the world's largest messaging application by active user count. It is an extraordinarily successful product. It is also, fundamentally, a messaging application — a tool for sending text, voice, and media between individuals and groups. Its value proposition is communication. Its competitive moat is the social network effect of having the people you want to communicate with already on the platform.

WeChat is not a messaging application that has added features. It is an operating system for daily life that happens to have originated as a messaging application. The distinction matters enormously for competitive analysis.

Within WeChat's ecosystem, a user can: communicate with individuals and groups; consume short-form video content through Video Accounts; read long-form articles through Official Accounts (公众号); make payments to individuals, merchants, and government services through WeChat Pay; access over 4 million mini-programs spanning e-commerce, food delivery, transportation, healthcare, financial services, and entertainment; search for information through WeChat Search; manage professional relationships through enterprise WeChat; and, increasingly, interact with AI agents capable of executing complex multi-step tasks by calling upon the mini-program ecosystem and payments infrastructure as native tools.

This is not a feature list. It is a description of a closed-loop digital economy in which WeChat functions as the primary interface between users and virtually every dimension of their commercial and social lives. The private domain ecosystem that WeChat has constructed — the combination of social graph, content infrastructure, mini-program tool network, and payments rails — represents a form of platform sovereignty that has no direct equivalent in Western internet architecture.

Meta's ecosystem, by contrast, remains structurally fragmented. WhatsApp handles messaging. Facebook handles social content and advertising. Instagram handles visual content and influencer commerce. Each application is powerful within its domain. None of them has achieved the cross-domain integration that would allow Meta to offer users a single interface for communication, commerce, content, and financial services simultaneously. The applications share user identity infrastructure and advertising targeting data, but they do not share a unified operating environment in the way that WeChat's mini-program ecosystem creates.

The Monetization Architecture

This structural difference has profound implications for monetization. Meta's primary revenue model is advertising — specifically, the sale of targeted attention to brands and performance marketers. This is a powerful business, but it is fundamentally a two-sided market in which users are the product and advertisers are the customer. The value Meta extracts from its social graph is mediated through the advertising market.

WeChat's monetization architecture is more complex and, in several respects, more durable. Advertising through Video Accounts and Official Accounts represents one revenue stream. But WeChat Pay generates transaction-based revenue from the commercial activity that flows through the ecosystem. Mini-programs generate revenue through the commerce and services they enable. The social graph itself creates distribution value for Tencent's gaming, content, and enterprise services businesses that would otherwise require expensive customer acquisition spending.

More importantly, WeChat's monetization is still in early stages relative to its structural potential. The Video Accounts ad load of 4.5% — against an industry benchmark above 20% — represents a deliberate choice to preserve user experience rather than a ceiling on commercial capacity. Management has explicitly acknowledged the "substantial headroom" available for ad load expansion. The mini-program ecosystem, with 4 million+ applications and 1 billion+ users, has barely begun to be monetized through platform fees and AI-enhanced discovery. The WeChat AI Agent infrastructure, once deployed, will create entirely new monetization surfaces that do not yet exist in the financial model.

The Switching Cost Architecture

Perhaps the most important structural difference between WeChat and Meta's ecosystem is the nature and depth of the switching costs each has constructed.

Meta's switching costs are real but primarily social: leaving Facebook means losing access to the social graph you have built there. These costs are meaningful, but they have proven surmountable — Facebook's user demographics have shifted significantly over the past decade as younger users migrated to Instagram and TikTok, demonstrating that social graph switching costs, while substantial, are not absolute.

WeChat's switching costs operate at a different level of depth. Because WeChat is not merely a social platform but a commercial and financial infrastructure, leaving WeChat does not simply mean losing social connections. It means losing access to the mini-programs through which users manage their daily commercial lives, the payment relationships they have established with merchants and service providers, the professional communication channels through which their work is conducted, and the content subscriptions through which they consume information. The switching cost is not the loss of a social network. It is the loss of a digital operating environment.

This is why the historical challengers to WeChat — Laiwang, Duoshan, Chatbao — failed not merely to displace WeChat but to achieve any meaningful adoption at all. They were competing against a messaging application in a world where WeChat had already become something far more than a messaging application. The competitive frame was wrong from the outset.

Structural Comparison

The table below summarizes the key structural dimensions of this comparison:

| Dimension | WhatsApp / Meta Ecosystem | |

|---|---|---|

| Core Function | Digital life operating system | Messaging + social content + advertising |

| Mini-Program Ecosystem | 4 million+ applications, native tool library | No equivalent infrastructure |

| Payments Integration | WeChat Pay, 1 billion users, native to ecosystem | Limited; relies on third-party payment rails |

| AI Agent Capability | Mini-programs as tool library; payments as execution layer | No equivalent closed-loop infrastructure |

| Switching Cost Depth | Social graph + commercial infrastructure + financial services | Primarily social graph |

| Monetization Headroom | Video Accounts ad load at 4.5% vs. 20%+ industry average | Advertising model approaching maturity in core markets |

| Competitive Moat Type | Social network effects + platform network effects + switching costs (compounding) | Social network effects + advertising scale |

Investment Implication

The conclusion that emerges from this comparison is not that Meta is a weak business — it is one of the most profitable advertising platforms in history.

The conclusion is that WeChat has constructed a form of competitive advantage that is structurally distinct from anything in the Western internet landscape, and that the standard frameworks developed to analyze Western platform businesses are insufficient tools for understanding it.

Relationships Over Users

The analytical journey through WeChat's competitive architecture leads to a conclusion that is simple to state but takes considerable rigor to fully appreciate.

Users Are Not the Moat

Every major technology platform in history has been built on users. Users generate the data, the engagement, the network density, and the advertising inventory that constitute the commercial value of a platform business. User counts are the primary metric by which platforms are evaluated, compared, and valued. The entire vocabulary of platform analysis — monthly active users, daily active users, time spent, user acquisition cost, lifetime value — is organized around the user as the fundamental unit of competitive advantage.

WeChat has transcended this framework. Its 1.4 billion MAU figure is not irrelevant — scale matters for network effects, and WeChat's scale is extraordinary. But the MAU figure is not the source of WeChat's moat. It is a consequence of it.

The More Rigorous Unit of Analysis

The source of the moat is the 1.4 billion × (average contacts per user) relationships that have been encoded into WeChat's social graph over fifteen years of daily use. These relationships — professional connections established at conferences, family bonds maintained across distances, friendships formed in university and preserved through decades of life change, commercial relationships between merchants and customers — are not portable. They cannot be exported to a competing platform. They cannot be recreated from scratch. They exist, in their current form, only within WeChat's ecosystem.

This is why the "后发制人" strategy works for Tencent and would not work for a company without WeChat's foundation. The strategy requires a distribution asset so durable that competitive displacement is structurally impossible regardless of how long the company waits before entering a new category. WeChat provides that asset. The social graph encapsulation ensures that users cannot leave even if they want to. The private domain ecosystem ensures that new capabilities can be deployed to the existing user base at near-zero marginal acquisition cost. The payments infrastructure ensures that commercial value can be captured from any activity that flows through the ecosystem.

The implications for how we evaluate Tencent's AI strategy, its Video Accounts monetization trajectory, and its cloud computing ambitions are significant and will be explored in subsequent chapters of this series. But the foundation for all of those analyses is the insight developed here.

Final Analytical Frame

The market counts users.

The more rigorous investor counts relationships.

When assessing the Tencent network effect, the temptation is to count users and call the analysis complete. The more rigorous approach — the one that explains why every well-funded challenger has failed, why the "late mover" strategy has succeeded repeatedly, and why WeChat's competitive position has strengthened rather than weakened over two decades of intense competition — requires looking past the users to what the users have built inside the platform.

They have built their social worlds.

And social worlds, unlike user accounts, cannot be migrated.

Final Thought

WeChat's moat is not users.

It is relationships.

And relationships, unlike users, cannot be migrated.

Tencent Research Hub

This article is part of the LongViewValue Tencent Research Series.

Published

✓ Tencent Investment Thesis

✓ Tencent Economic Moat (Current Article)

Coming Next

→ Tencent AI Strategy

→ Tencent Capital Allocation

→ Tencent Valuation

← Back to Tencent Research Hub

Continue Reading

The next articles in this series will examine Tencent's AI strategy, capital allocation discipline, and valuation framework in greater detail, including Owner Earnings quality, Free Cash Flow generation, ROCE sustainability, Sum-of-the-Parts valuation, and the AI optionality embedded in the current market price.

Disclosure & Disclaimer

LongViewValue publishes long-form investment research for sophisticated long-term investors.

This article is provided for educational and informational purposes only. It does not constitute investment advice, investment research, a securities recommendation, or an offer to buy or sell any security.

All analysis reflects the author's independent views based on publicly available information and may contain errors, omissions, or outdated assumptions.

Investors should conduct their own independent research and consult qualified professionals before making investment decisions.